Fuelled by record transaction volumes and an influx of institutional capital, 2025 saw the resurgence of Big Gun shopping centres as a central focus in Australian retail investment.

The Australian retail property market experienced a seismic shift in 2025, with Big Gun shopping centres firmly returning to centre stage. These fortress-like assets possess the power to influence entire markets and redefine investment approaches when they change hands. The sector experienced an exceptional 12 months characterised by unprecedented transaction volumes, renewed institutional investor participation, and a worldwide resurgence that has positioned Big Guns at the forefront of investment appetite.

![]()

A record year for Australian retail

Total retail property transaction volumes reached $13.5 billion in 2025, representing a 56 per cent increase on 2024 volumes and sitting 87 per cent above the 10-year average, driven predominantly by shifting global sentiment and a gradual reweighting towards the sector by capital sources. For the first time on record, retail emerged as the highest-traded real-estate sector nationally, outtrading both the office and industrial sectors. This underscores the sector’s resilience and signals a fundamental shift in capital allocation strategies.

The driving force behind this record performance was undoubtedly the Big Guns sub-sector (centres with more than 50,000sqm in GLA). Big Gun assets delivered an unprecedented $6.9 billion in transaction volumes across 12 deals, a 75 per cent increase over the previous high in 2020 and representing 51 per cent of total retail transactions throughout 2025. To put this in perspective, Big Guns have represented only 15 per cent of total annual retail property volumes, on average, over the past 10 years.

Benchmark transactions reshape investment landscape

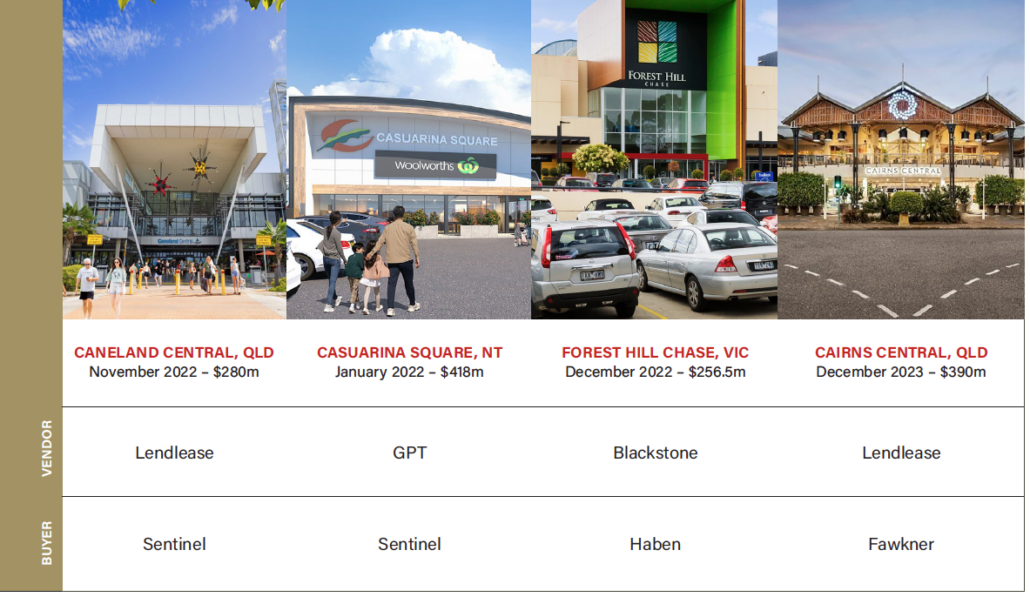

The year was anchored by several landmark transactions that exemplified the sector’s transformation. Erina Fair’s $895 million sale to Fawkner Property Group at a 6.25 per cent market yield became the year’s standout transaction as Australia’s largest single asset sale in history by dollar value, while Top Ryde City attracted attention through its $525 million acquisition by Keppel REIT (75 per cent) and MA Financial (25 per cent), marking the Singaporean REIT’s debut Australian retail investment. Woodgrove Shopping Centre’s $440.5 million sale to Assembly Funds Management further reinforced pricing resilience across the sector.

Nick Willis, Executive Director of JLL Retail Investment Australia and New Zealand, notes,”We are witnessing a significant global shift as major institutional investors now reconsider the retail sector. After more than a decade of largely stepping back, many of the institutions that once underwrote this market are actively looking to re-enter.Domestically in Australia, this resurgence has been spearheaded by superannuation funds, which have deployed over $4 billion into retail property globally in the last 12 months, with substantial additional commitments on the horizon.”

Westfield Sydney’s partial stake sale marked another watershed moment, with QIC led Australian Retirement Trust mandate (ART) acquiring a 19.9 per cent interest for $864 million, reflecting a 4.69 per cent market yield, reaffirming the capital demand for true core real estate. This transaction was particularly significant as it represented QIC’s new mandate’s (ART) first foray into Big Gun direct ownership and demonstrated the appetite for premium assets among Australia’s largest superannuation funds.

Other notable transactions included the sale of a 50 per cent stake in Macquarie Centre for $830 million to Cbus and UniSuper, and Westfield Chermside’s dual 25 per cent tranches ($683 million each, sold to Dexus). Additionally, the two Big Gun assets involved in GPT’s fund transactions – a 50 per cent interest in Rouse Hill Town Centre and Highpoint Shopping Centre – traded for $395 million and $204.6 million, respectively. Of the 12 Big Gun transactions to occur in 2025 only three were via public campaign, underscoring the tightly guarded nature of these trophy assets.

The return of institutional capital

Perhaps the most significant development of 2025 was the re-emergence of institutional capital as major participants in Big Gun ownership. After years of syndicator dominance, pension funds, wholesale funds, and REITs returned to the market with renewed vigour. Institutional buy-side activity in retail was up 90 per cent over the 5-year average, with $5.7 billion purchased by institutions across all retail sub-sectors in 2025. Both Big Gun and Little Gun centres have been re-institutionalised, with institutional capital buying 158 per cent more Big Guns and 82 per cent more Little Guns versus the past five years.

During the past five years, syndicators accumulated more than $7.6 billion worth of Big Gun assets, representing 42 per cent of all acquisitions within the Big Gun market. Last year, traditional institutional players reasserted their presence, representing 56 per cent of all Big Gun acquisitions.

This institutional re-engagement represents a significant shift from the syndicator-led landscape that has characterised the market since 2020, evidenced by the three historical syndicator-led transactions above.

New partnerships have emerged as a key theme, with joint ventures between superannuation funds (such as Cbus & UniSuper’s Macquarie Centre acquisition) and cross-border alliances (like MA Financial & Keppel REIT’s Top Ryde partnership) becoming an increasingly common occurrence.

Sam Hatcher, Head of Retail at JLL adds, “The bottom-up fundamentals are attracting capital. Three years of consistent occupancy improvement and increasingly favourable re-leasing spreads have proven these assets can deliver through choppy economic conditions. What we’re observing in deal processes is a marked shift in buyer composition, fewer opportunistic players and the return of traditional institutional capital to the sector. The challenge now is access to productive assets. With so few assets trading publicly, in particular controlling interest, we anticipate 2026 will see the birth of many new partnerships.”

What’s driving current retail sentiment?

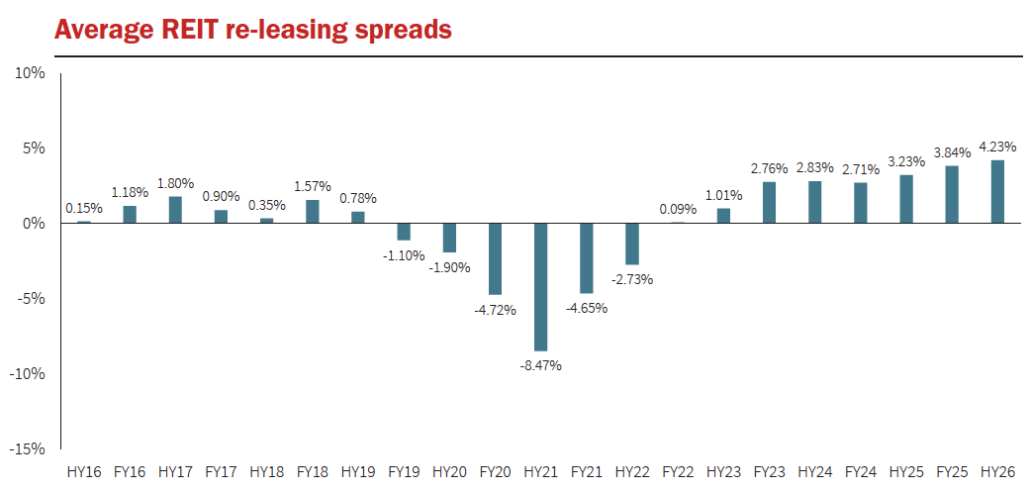

The resurgence of Big Gun trading is underpinned by three consecutive years of strengthening fundamentals that have shifted investor sentiment. Re-leasing spreads have emerged as a particularly compelling indicator, averaging more than 3.84 per cent across major REITs in 2025, the highest level on record and representing the third consecutive financial year of positive re-leasing spreads. This performance has been complemented by significant compression of vacancy rates, which fell from 4 per cent in 2020 to just 2 per cent in 2025*, while population growth remains robust at 1.5 per cent annually as new retail supply declines.

Taking a step back, the majority of investment groups remain underweighted to the retail sector. Globally, MSCI states, investors maintain only a 12 per cent weighting towards retail, compared with 20 per cent for industrial assets and 25 per cent for office. Domestically, JLL data shows this imbalance is even more pronounced, with office assets having accumulated $85 billion in excess transactions since 2010, implying a 2:1 ratio of investment volumes between office and retail over the last 15 years. The last five years, however, have shown signs of change, as transaction weightings have rebased, with retail the most traded sector for the first time on record in 2025**.

As volatility persists in other commercial property sectors, retail fundamentals imply confidence in the continued re-weighting towards retail, which aids in exit underwriting for current assets and supports forecast capital growth as more investment groups seek exposure to the sector.

![]()

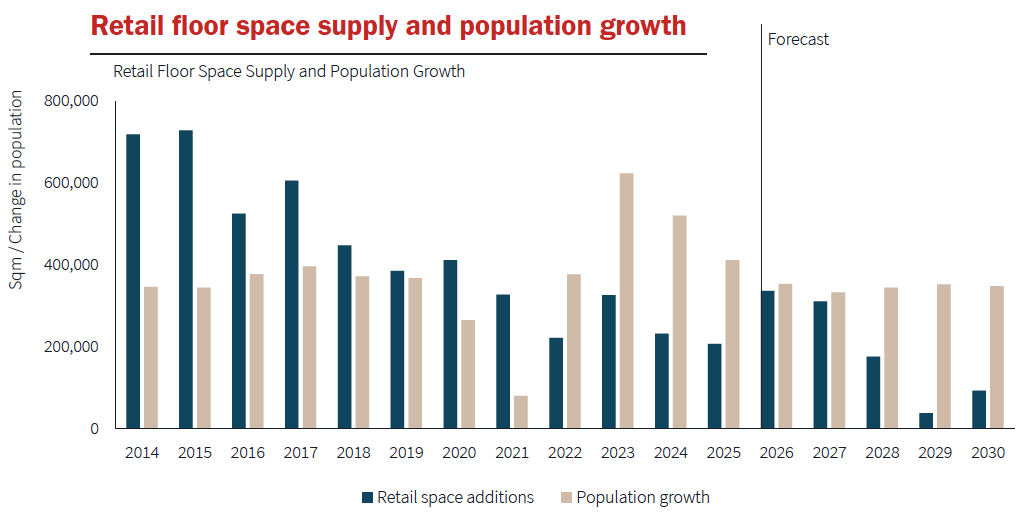

The floor space supply-side constraints further amplify this investment case. The feasibility of building new retail assets of scale remains at an historical low, with new regional centre development representing less than 5 per cent of all new retail space from 2020-25, compared with 15 per cent from 2010-15. This dramatic decline in new supply creation has intensified competition for existing assets, particularly those with dominant market positions and strong tenant covenants. With population growth set to outpace retail space additions, Australia requires an estimated 38 Big Gun-scale centres by 2030, in a mid-case scenario, to maintain current floor space requirements on a per capita basis; however, the pipeline for this scale of asset remains close to empty.

In an environment where a cycle of higher interest rates may affect terminal yield assumptions across commercial property, asset classes like retail, that combine limited floor space supply with strong underlying fundamentals, are likely to be favoured by investors. The sector’s demonstrated ability to deliver rental growth provides a natural hedge against rising rates, positioning Big Gun assets as particularly resilient in changing monetary conditions.

Retail trends

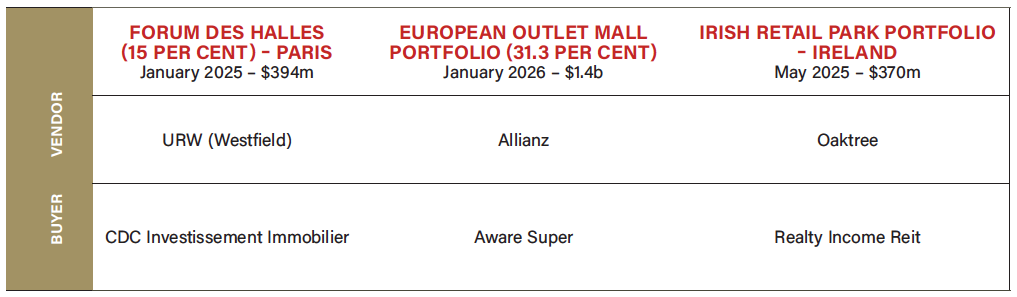

The success of the retail sector is not just a domestic story. Globally, retail transaction volumes are 15 per cent above the prior five-year average as sales of Big Gun-size assets have been more prominent across major global economies. European activity has been particularly noteworthy, with URW making its first major acquisition since 2019, providing a vote of confidence in the market. Australian superannuation funds have also begun looking internationally, with Aware Super taking a 31.3 per cent stake in a European outlet mall platform, driven by tight Australian supply, global diversification and growth ambitions.

Conclusion

Last year will be remembered as the year Big Guns truly returned to prominence in the Australian retail investment landscape. Record transaction volumes, institutional capital re-engagement, and robust fundamentals have combined to create an environment of renewed confidence and competition. However, the increased activity has made it increasingly difficult for capital to gain access to this asset class, with groups that previously sought 100 per cent ownership now looking at partial interests as an alternative strategy, a thematic expected to continue throughout 2026.

The timing appears particularly favourable for prospective investors, as some of the funds that acquired assets over recent years are now looking for exit opportunities, with a substantial wave of recycling capital expected within the next 24 months. This coincides with continued yield compression driven by improved fundamentals, capital reweighting, and an intensifying supply-demand imbalance.

The structural themes supporting this recovery – limited supply, growing population, improving retail performance, and sustained capital underweighting – remain firmly in place as we progress through 2026. With heightened competition, deeper liquidity pools, and an increasing focus on partial transactions, the Big Gun sector appears well-positioned for continued strength. The question now is not whether Big Guns will remain in favour, but rather, who will be the new entrants capable of accessing these tightly held assets in an increasingly competitive marketplace. Will you buy a Big Gun this year?

- This article by James Hayward and Sam Linden of JLL is published in SCN magazine – Big Guns 2026 edition.

*According to JLL research vacancy data for Regional Centres

** JLL records date back to 2007

Add comment