For decades, Australian retail investment followed a familiar playbook. Long leases, newly built assets and supermarket anchors were prized for their predictability. Smooth valuation models, stable cashflows and straightforward financing defined what “quality” looked like.

That logic no longer dominates buyer thinking.

Today, investors seeking enhanced returns are deliberately targeting short Wale (Weighted Average Lease Expiry) retail assets – not despite the risk, but because of the opportunity it creates. Lease expiry, particularly for the anchor supermarket tenant, is no longer something to de-risk ahead of a sale. In many cases, it’s the entire point of the investment thesis.

This shift reflects a more sophisticated view of retail real estate: One that values flexibility, optionality and land fundamentals just as highly as income security.

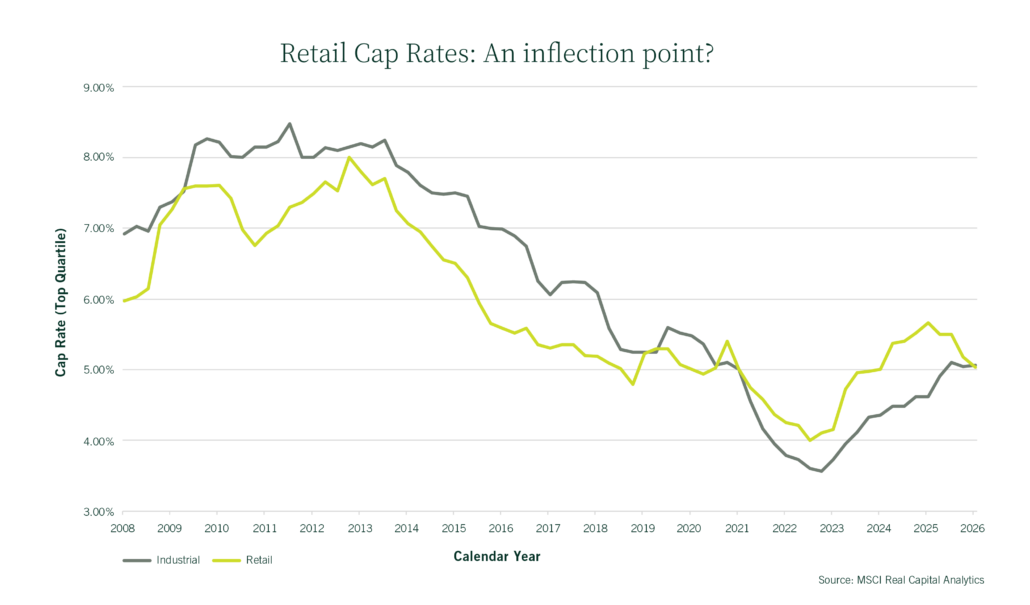

Is retail becoming the next industrial?

What we’re seeing in retail today echoes the industrial sector’s evolution between 2021 and 2023.

It was in that period, the strongest demand was for properties with short leases, minimal options and under‑rented income streams. As leases expired, rents rebased sharply, pushing total returns well ahead of expectations and driving aggressive yield compression. Prime yields compressed to below 4 per cent. Total returns reached 19.2 per cent in the 12 months to Sep 22.

Retail is now following a similar path. In strong catchments, investors are underwriting lease expiry risk with far more confidence than they would have historically, particularly where underlying land value, population growth and tenant demand support future income growth.

“Income flexibility, not income certainty, quickly became the most valuable attribute in industrial property and we are seeing the signs of retail following a similar trajectory,” said Philip Gartland, national partner.

A structural shift in retail

“The fundamentals underpinning the retail renaissance are well documented. The difference is we are now seeing these fundamentals expressed in rental levels and asset pricing,” said Carl Molony, national partner.

- Population growth: 1.6 per cent annual population growth.

- Spending growth: Retail sales rose 4.9 per cent YoY.

- Low unemployment: 4.2 per cent unemployment.

- Construction costs: 5 per cent increase in Sydney through 2025.

- Scarcity of retail-zoned land: Well-located retail land is finite, tightly held and well protected through planning controls. Retail undersupply of approximately 2.2 million sqm projected by 2032.

- Density: Ongoing housing undersupply is accelerating higher‑density living around town centres – exactly where retail land already exists and where mixed‑use outcomes can be unlocked. Nationally, the gap between housing demand and delivery has exceeded 240,000 homes over the past three years.

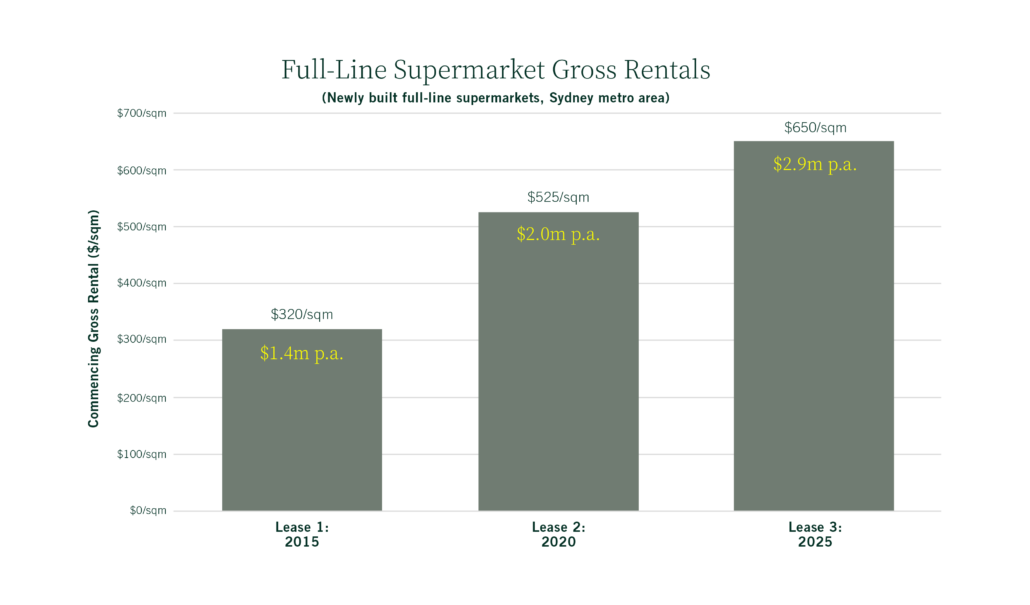

Supermarket rents: The clearest signal of change

No part of the retail market better reflects the shift than supermarket rents.

Over the past decade, supermarket tenants have materially recalibrated what they’re prepared to pay for the right sites, particularly in strong, supply‑constrained catchments. In many cases, rents agreed today bear little resemblance to those set under legacy leases signed in the early 2000s or 2010s.

By comparing three new-build Sydney supermarket leases from 2015 to the present, the change becomes clear. Whilst every site, location and catchment are unique, these examples demonstrate the potential upside for centres that roll out of ‘old’ legacy leases into the new market reality.

The benefits of short Wale – for both landlords and tenants

Retail and town centres are living assets. Customer behaviour, tenant formats and space requirements evolve continuously.

Long-term leases with multiple options can freeze that evolution. Some centres have been unable to evolve, due to being locked into 20–40-year tenure via long-term major tenant leases. These deals have meant both landlord and tenant have been unable to evolve their offering, and the expiry creates a rare opportunity to reset and position for growth.

What are the opportunities with short Wale assets?

- Centre upgrade: Lease expiry creates alignment to reinvest in stores, amenities, plant and public realm improvements, often with direct performance benefits for the tenant.

- Omnichannel retail: Click‑and‑collect, last‑mile logistics and in‑store fulfilment are now part of standard retail operations. Short Wale assets allow physical space and lease terms to adapt, creating opportunities to improve tenant performance and update turnover rent provisions.

- Car park control: Long major tenant leases typically include strict car parking ratio and control provisions. Regaining this control can drive outstanding outcomes for both landlord and tenants. Improving circulation, new pad sites, shade sails, EV chargers and solar solutions become possible.

- Conversion: Besides supermarkets, other big box uses like hardware or discount department stores also offer huge potential at expiry. Some of the strongest returns we’ve seen in recent years have come from converting a vacated Bunnings box to multiple LFR stores & logistics facilities or converting low-rent DDS space into online fulfilment.

- Reversion: Significant rental reversions are possible across all retail types, but particularly for centres with legacy major leases. By working closely with the major tenant to drive centre and tenancy enhancements at renewal, landlords can achieve a strong uplift in income and tenants can enjoy enhanced performance and sustainable revenue growth.

- Mixed-use: Well-located retail land is ripe for mixed-use development and increasingly important to deal with residential supply shortages, particularly in metropolitan locations and/or those that benefit from transport adjacency. Short Wale assets provide the protection of short-term income whilst planning and approval phases can be completed for mixed-use development. The ability to secure a major tenant to underpin a mixed-use development is attractive, as it reduces the reliance on residential pre-sales to underpin finance.

The results – pricing tells the story

Stonebridge has recently transacted several landmark short-Wale retail assets, including Caringbah Village, the former Bunnings at Campbelltown and Gladesville Village.

Across these campaigns, several consistent themes emerged:

- Buyer depth was exceptional, spanning passive investors, value-add capital, developers, land bankers, owner-occupiers and special purchasers (major tenants/owner occupiers and surrounding landowners).

- Passing yields were not the focus. Buyers were prepared to underwrite low initial returns where the reversion or value add story was compelling.

- Mixed-use developers were among the most active bidders, particularly where planning and density fundamentals aligned.

The landlord playbook: Why de-risking before sale is no longer the default

Historically, there was a tendency for landlords to renew leases with multiple options to de-risk an asset before taking it to market. Now, buyers covet flexibility to capitalise on the tailwinds in retail, and tenants want to constantly evolve their offering to adapt to the changing retail environment.

So, in strong locations with strong performing centres, don’t be afraid of short Wale – as an increasing number of purchasers and their financiers are embracing it. It can unlock superior asset outcomes and superior returns, where the dynamics are favourable.

About Stonebridge

Stonebridge Property Group is Australia’s leading owner-operated commercial real estate agency.

Stonebridge specialises in the sale, leasing and management of shopping centres, freestanding investments and development sites across Australia and New Zealand and transacts over $3 billion in real estate per annum.

- Visit www.stonebridge.com.au to find out more.

Add comment