Through interviews with leading experts in planning, economics, and leasing, Joseph Wright from i2C Architects unpacks the ‘growth areas paradox’, offering critical insights into development viability, changing retail dynamics, and the future of town centres in growth corridors.

Amidst a backdrop of ambitious planning changes in Victoria and around the country that focus on accelerated housing affordability and employment, it feels like an important time to discuss what this might all mean for the development of smaller towns further out in our growth corridors. In Victoria, through the initial Activity Centre Program (ACP) that was launched a few years ago, we’ve witnessed a transformation proposed for the business and retail cores in the first 10 pilot suburbs within metropolitan Melbourne.

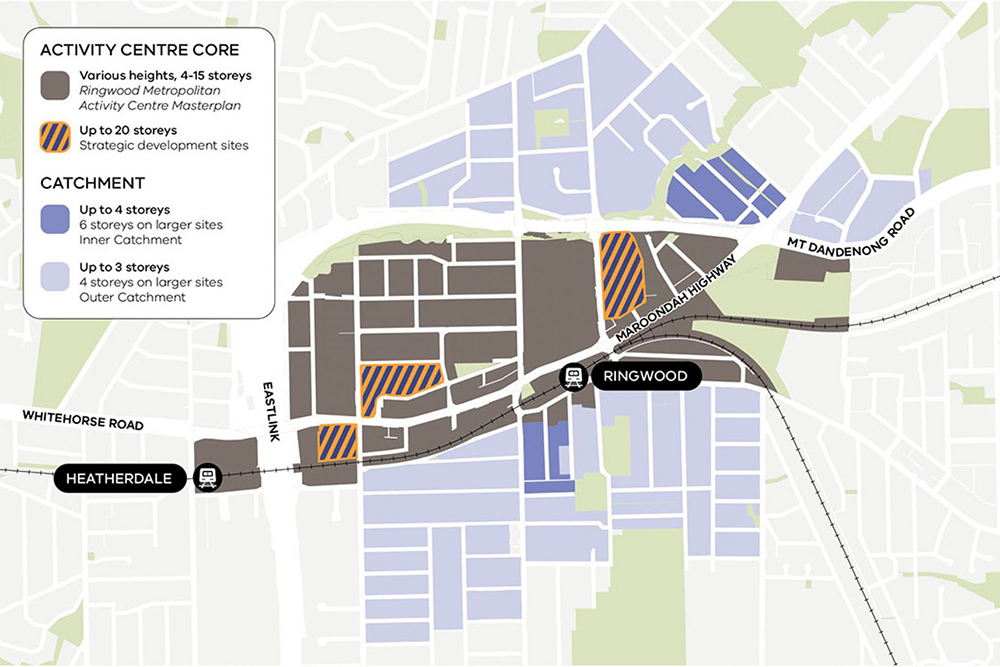

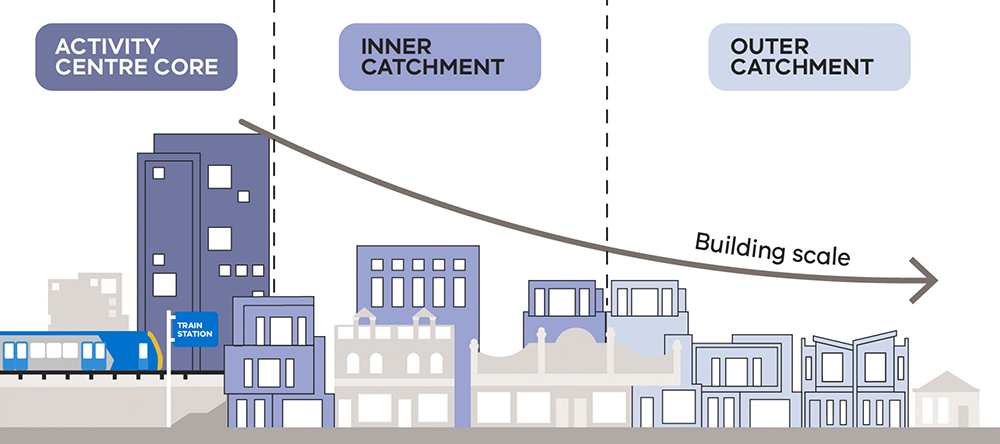

The plan for Ringwood for example, encourages medium and low-rise buildings within the inner and outer catchments of 3-4 storeys, taller buildings within the activity centre core of 4-15 storeys, and additional 20-storey buildings in strategic development sites in the activity centre core.

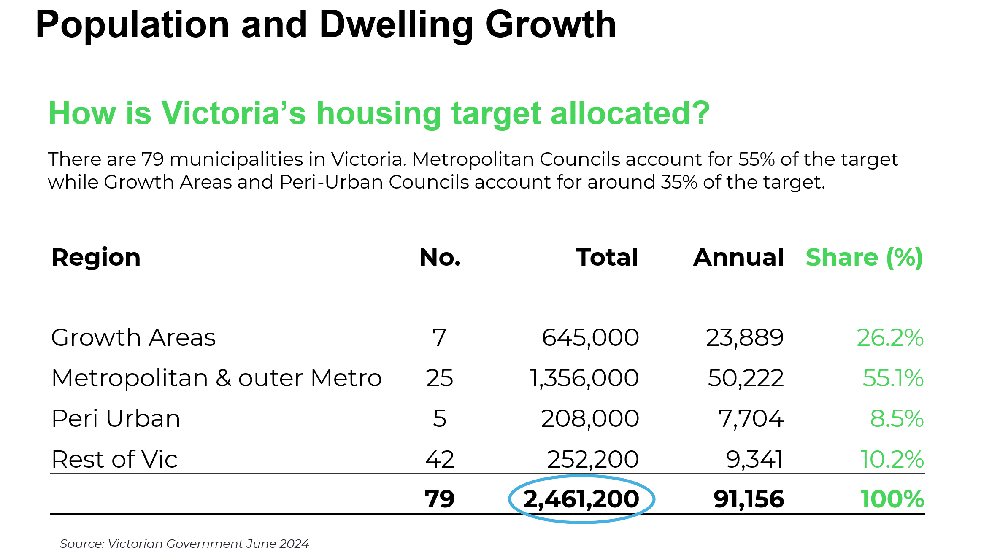

This speed of change is a pivotal ingredient in reaching the target of 300,000 new homes in and around targeted activity centres by 2051. As set out in the Plan for Victoria 30-year strategic land-use guide, we’re now beginning to see the ACP expand to include an additional 50 ‘train and tram’ zones to reach a target of 1.8 million new homes in the next 25 years across metropolitan Melbourne and 2.24 million homes across Victoria.

Reflecting on the above, it can be difficult not to consider what the pace of suburban life in Melbourne might feel like in the near future. Does the sense of ‘local’ become lost in the context of multi-programmatic large-scale developments? And what role, if any, do the growing new communities in our outer areas play in supporting population growth and in defining Australia’s suburban identity for future generations?

Looking beyond the aesthetics to unpack this, this article summarises interviews conducted with Michael Henderson from Contour Planning and Advisory (MH), Brian Haratsis from Macroplan (BH), and Patrick McFadden from Accord Retail Leasing (PM) – three leading town-centre experts in the fields of planning, economics and leasing, respectively.

Joseph Wright: Regarding Victoria’s housing targets, what role do you see the growth areas playing in reaching them?

BH: Growth Areas and peri-urban councils were forecast to account for 35 per cent of the target – they’re performing at 55 per cent at the moment. So in terms of keeping pace with population growth, the growth areas are growing faster than expected.

MH: Agree with the comments from BH, and in many respects, the planning framework has been set up to allow for the Growth Areas to be a “supportive role”, with metropolitan areas still required to do the heavy lifting.

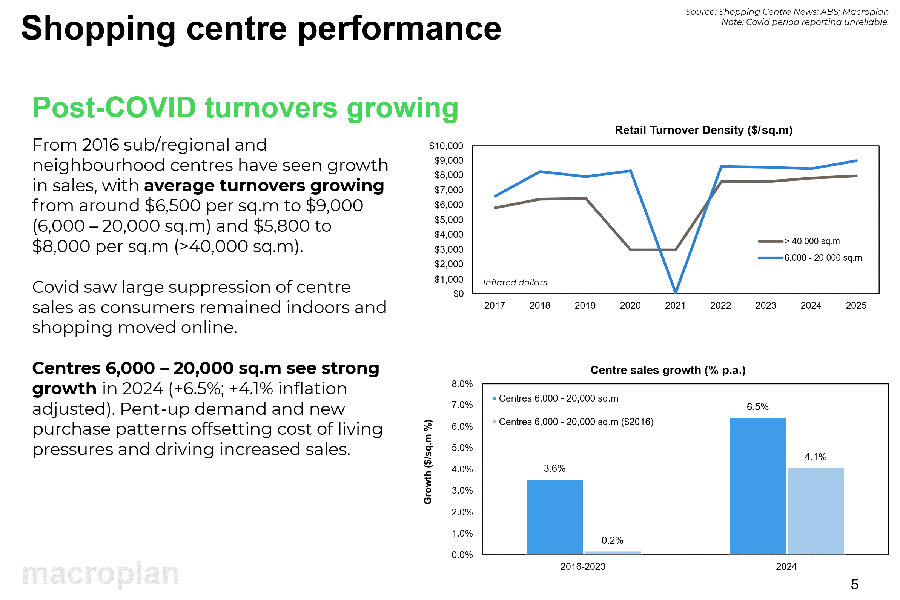

JW: The data indicates that the sub regionals and neighbourhood centres have seen strong sales growth over the past 10 years. What do you think is driving that?

MH: Philosophically, there is a shift under way in how people live, work and shop. It started before Covid-19 but has accelerated greatly.

State planning policy consistently reinforces:

- The hierarchy of centres

- The scale/density that surrounds these centres

- The establishment of “20-minute neighbourhoods”, which are largely targeted for sub-regional settings.

BH: A supply shortage for sure, because there simply aren’t enough centres to go around and that’s the key driver, but also in the growth areas – a key driver is working from home.

PM: We’re also simply seeing fewer vacancies in a lot of the smaller shopping centres. In the past, a lot of these centres might be carrying one or two vacancies and we’re seeing fewer like that now. So the more shops that are open, the more sales are getting done, too.

BH: With more working from home, there’s just more demand and, combined with a lack of supply, you get fewer vacancies.

JW: Within growth areas, the data suggests, more people aren’t necessarily working from home though?

MH: Agreed, thus my reference to ‘philosophically’ above. It is important to remember that growth areas ‘house workers’, and the demographic of residents to access this housing type is an important factor.

BH: That’s right – in growth areas, you haven’t got as many professionals, but a greater percentage of professionals that have to work on site – like school teachers, nurses, policemen, etc. So you don’t get as much work from home, but the people that can work from home, work more hours from home.

JW: Is there any concern that online shopping will reduce bricks-and-mortar shopping in the future?

PM: In a lot of these areas, it’s typically more food and service retailers anyway. However online shopping is accounting for more than 10 per cent of sales for a lot of the supermarkets now.

BH: Typically, supermarkets are doing 5-10 per cent of their sales online and I’m not assuming a huge increase. The rate of growth will slow down, but we will see a greater percentage. It will probably approach 20 per cent over time, maybe 25 per cent in 10 years’ time – it’s 25 per cent in Britain now.

MH: Would be interesting to see how the global rates of online purchase compare with those that have a climate similar to Melbourne’s, and how, if at all, this influences online purchasing.

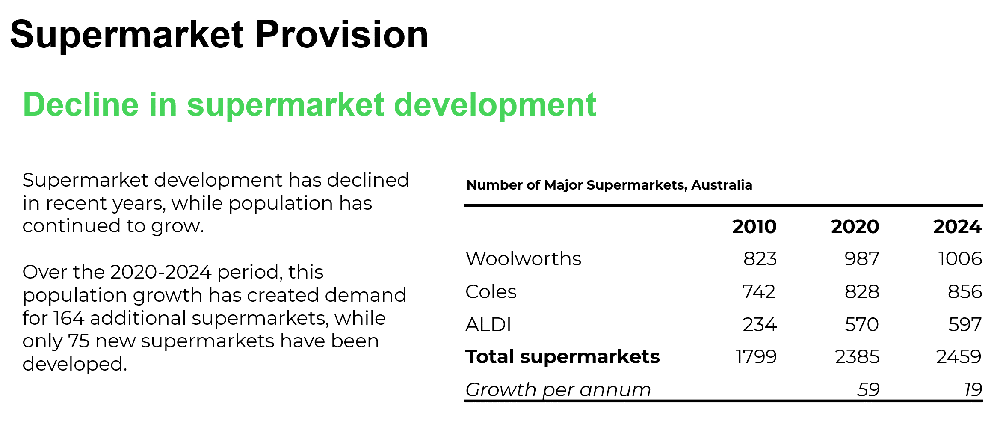

JW: The data highlights a decline in the number of supermarkets being developed nationally, from 59 stores in 2020, to just 19 in 2024. What impact do you see this having on the development of town centres in the growth areas going forward?

MH: Significant. Supermarkets are a keystone for the success of growth areas in respect to employment generation, they provide for a sense of destination and they are often a trigger for the broader activity centre being delivered.

BH: During the 2020-24 period, population growth has created demand for 164 additional supermarkets, while only 75 new supermarkets have been developed. So if you have fewer supermarkets, you’ll have fewer specialty shops. Centres with 10 or 12 specialty shops is where we’re headed.

JW: What leasing trends are you seeing in the growth areas?

PM: Essentially, there’s a lot more demand for food. Crews like Victoria’s Pizza ‘N’ Beyond and Burger Road, which have about 10 stores now, are ideal for these developments. Laundromats also, where people are often after a simple type of business they can operate close to home.

JW: Regarding that demand for food tenancies, are you seeing it being limited more toward smaller operators?

MH: We often muse within the office as to how many cafes a particular activity centre can have, irrespective of metropolitan or regional setting.

PM: That’s right. The issue you run into constantly (with larger food tenancies) is the cost of fitouts – Category 1 works being through the roof and scaring people off.

JW: Finally, what do you see as the biggest challenges facing developments in growth areas?

MH: It must be said that cost escalation remains a key challenge raised by our clients, but more broadly, from a planning perspective, two key challenges come to mind:

- Uncertainty of infrastructure delivery is creating a confidence and viability issue.

- Although some key planning reforms over the past few years have made part of the planning process easier, the effort and energy required to manage the planning permit process continues to increase. Consultant teams are getting bigger, the planning controls are becoming increasingly complex and cumbersome (bushfire, cultural heritage, public acquisition), while it seems that government stakeholders are often under-resourced.

PM: The only negative is there’s not enough supply. In some ways, it’s actually a positive that with less NACs available, I’ve got constant enquiries for all the centres I’m leasing at the moment. So we’re able to be a little more selective with who we put in.

BH: Melbourne is growing faster than South-East Queensland at the moment, so we’re the fastest-growing town in Australia. With 102,000 people last year, it’s faster than Sydney, faster than Brisbane, faster than anywhere in Australia, and yet there’s a very limited amount of development. At the moment, there are a number of centres that aren’t good enough and there are too many centres in some locations and not enough in others – so my advice is do your research.

- This exclusive interview by Joseph Wright, Design Director at i2C Architects is published in the latest issue of SCN magazine – Big Guns 2026 edition.

Brian Haratsis – Macroplan (CEO)

Brian established Macroplan in 1985 after gaining experience in local government, state government and private consultancy. Brian is a recognised industry leader and Fellow of the Planning Institute of Australia and Victorian Planning and Environmental Law Association, holding positions on several Property Council of Australia Committees. Brian is an economist, strategist and adviser with more than 40 years of experience in urban economics and planning in Australia and internationally.

Patrick McFadden – Accord Retail Leasing (Director of Leasing)

Patrick has more than 30 years of experience working with property owners & developers in developing retail mix, budgets and leasing strategies that have delivered optimum results for all stakeholders. An experienced retail leasing executive with a comprehensive background in retail planning, development feasibilities, tenant banking, retailer relationships and project delivery.

Michael Henderson – Contour Consultants (Director)

Michael joined Contour in 2018 and has been working as a town planner in both the private and public sector since 2008, holding senior positions at a number of government organisations. Michael brings detailed understanding of Victoria’s planning system and its intricacies to a wide cross-section of development projects. His expertise includes advice during site acquisition and project design, management of applications and negotiating successful approval outcomes with planning authorities.

References:

Victoria State Government (2025). Train and Tram Zone Activity Centres.

Victoria State Government (2025). Planning for a Thriving Ringwood.

Macroplan (2025) Retail in the Greenfields. Victorian Housing Targets: Data sourced from Victorian State Government 2024

Macroplan (2025) Retail in the Greenfields. Centre Sales Growth/Number of Major Supermarkets: Data sourced from Shopping Centre News/ABS/Macroplan

Macroplan (2025) Retail in the Greenfields. Centre Sales Growth: Data sourced from Shopping Centre News/ABS/Macroplan

Add comment