In this article for SCN magazine, JLL research analyst Holly Irvine explores how a new wave of international beauty, food, and luxury brands is transforming Australia’s CBDs into vibrant experiential hubs.

Central Business Districts (CBDs) represent the life, entertainment and culture of the cities they anchor. Strong domestic and international tourism means Australian CBDs are among the busiest internationally, attracting particularly robust visitation from key APAC markets. This consistently ranks Australia as a leading urban destination for leisure and business travel.

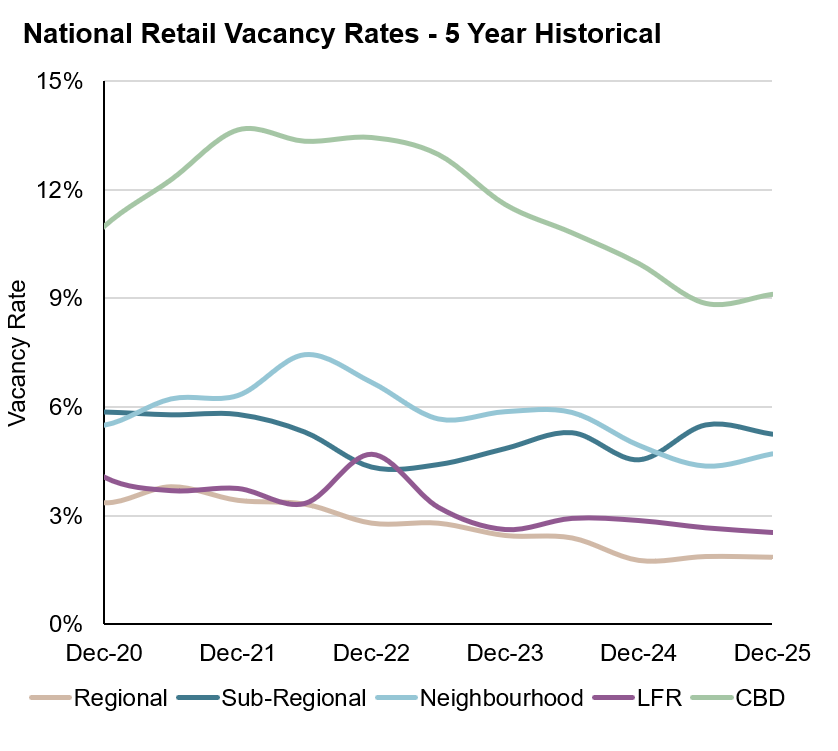

Both national and international retailers are attracted to Australian CBDs due to their centricity, accessibility and destination appeal. International retailers lift visitation, sharpen precinct identity and reinforce investor confidence in CBD retail real estate. JLL data shows CBD retail vacancy across Australia tightened to 10.3 per cent in the second half of 2025, with prime markets such as Sydney dropping to 3.4 per cent, as retailer demand continues to improve.

Past patterns, future insights

Zara is one of Australia’s most successful international retailers, opening its first store in Sydney’s Pitt Street Mall, which was closely followed by a second in Melbourne’s Bourke Street in 2011. At the time, the launch was described as “bringing foot traffic to a halt” as hundreds queued outside for novel European apparel. Since its first CBD openings, Zara has expanded to have 20 stores Australia-wide, its expansion highlighting that CBDs will often form a barometer before expansion into other markets occurs.

Around the same time, MUJI came to Chadstone, Japan’s Uniqlo opened in Melbourne’s Emporium, Sweden’s H&M opened at Melbourne GPO, and Louis Vuitton opened at George Street Sydney. This collective entrance of major international brands was not coincidental but a strategic choice of the Australian economy, which had comparatively emerged unscathed from the 2008 GFC. Australians embraced these arrivals, excited by new and different fashion concepts. These brands are all now embedded in the Australian retail landscape, surviving the test of time and demonstrating the sustained demand from Australian consumers long after the initial hype died down. International brand entry into Australia has remained stable since this heightened period.

How smart brands turned crisis into growth

Strong performance in the Australian market has driven many international brands to expand their store footprints across multiple CBD locations. Opportunistic companies capitalised on pandemic-induced, weaker CBD leasing environments to acquire a greater retail space at historically low rents per sqm.

Uniqlo expanded its Emporium Melbourne CBD store in late 2025, increasing its floor area by 110 per cent to now occupy 4590sqm. From the street, the four-floor store gives off a distinctly international feel, with its unmissable red square branding an homage to its Japanese origin.

The 2011 wave of international retail entrants was led by fashion; fast forward 15 years, to 2026, and the momentum sits with beauty, food and luxury retailers, all of which incorporate experiential in-store aspects.

The experience economy

Brand building used to be a slow simmer. International awareness grew gradually through travel, traditional media, and pop-culture osmosis. Today, social media has compressed discovery timelines dramatically. Australian audiences encounter brands through not only traditional store fronts but also through increasingly online exposure. This trend is reflected in e-commerce’s growing share of retail trade, expanding from 9.9 per cent in 2020-21 to 11.8 per cent in 2024-25.

Yet paradoxically, as e-commerce makes international products instantly accessible, physical brand launches in Australia have become more popular due to their elaborate nature, which consumers have come to expect. Experiential international CBD entrances deliver something digital channels cannot replicate, the visceral impact of in-person discovery. CBD locations serve the dual function of providing retail experiences and platforms for marketing. The media attention, foot-traffic and social-media content generated by a high-profile CBD opening creates a ripple effect that amplifies brand presence.

In this evolving landscape, the CBD flagship isn’t competing with digital, it’s completing it, transforming online buzz into strong foot traffic that benefits all surrounding retailers. Contrary to expectations, Gen X remains strongly in-store oriented, with 77 per cent preferring physical retail locations.

International beauty

The beauty sector has evolved from occasional discretionary spending to a regularly visited, highly engaging category rooted in wellness and daily habits. Australia’s cosmetics and toiletries retail sector has demonstrated robust growth, expanding from $4.4 billion in 2007-08 to a projected $6.3 billion in 2025-26, a 43 per cent increase over the period.

The Hailey Bieber-founded brand ‘Rhode’ launched into Australia via MECCA’s Bourke Street Melbourne and George Street Sydney in 2026, representing a compelling example of brand hype and market reach that only CBD locations can provide. Thousands of fans queued for hours, drawn by the opportunity to see Hailey Bieber; skincare and makeup products sold out. The oversized Rhode products in many local MECCA window displays carried a distinctly American sense of grandeur, and Australian consumers responded enthusiastically to this internationally flavoured experiential retail.

Beauty brands MECCA (which has a 21 per cent share of the Australian market) and Sephora (6 per cent market share),6 along with W Cosmetics demonstrate a broader shift in how international brands are entering the Australian market. Rather than rolling out stand-alone stores, many are choosing to enter through established platforms that have loyal customer bases, substantial market share and operational scale, plus are in strong-performing centres or prominent strips.

W Cosmetics is unique in its positioning, acting as a gateway through which Australian consumers can access Asian and, in particular, Korean skincare products that are not sold more widely.

Launching through major retailers also offers entry into strategic CBD locations that maximise visibility and foot traffic. Australia’s population is centralised around its CBDs with 88.1 per cent of the population nationally in urban areas. Relative to the UK (83.5 per cent) and US (84 per cent) Australia presents a unique and de-risked option for retailers expanding into our market. The ABS has reported that the most densely populated areas in Australia are Melbourne’s CBD, at an astounding 43,300 people per sq km, and Sydney Haymarket (CBD) 22,900 people per sq km.

This high population density explains how MECCA’s three-storey Bourke Street flagship, which opened in August 2025, was able to draw an estimated 20,000 customers on its first day and why international brands see the advantage of selling through distributors.

International food

Food and beverage have emerged as the strongest retail leasing category in Australian CBD precincts. Along Melbourne’s CBD strip retail, F&B operators have grown from 20 per cent to nearly 30 per cent of all retailers since 2021, with continued growth expected. The diverse food of CBDs reflects Australia’s multicultural landscape, with everything from bubble tea and hot pot to steak houses and French fine dining readily available. For younger adults, particularly those aged 25 to 34, weaker discretionary incomes are prompting more frequent fast-food purchases as an affordable and efficient dining option.

In 2025, Wing Stop entered Australia in Sydney’s CBD after going viral on Tik Tok through food reviews. The US Buffalo-style chicken wings restaurant had lines queuing around the block, with people waiting up to seven hours to try the 12 wing flavours. The first 500 customers received five free wings as part of the experiential launch strategy, creating excitement and encouraging trial.

Australia is also viewed as an attractive flagship-and-test market for brands that want visibility, trial and, if successful, permanent tenancy.

New York’s hugely popular burgers brand ‘Shake Shack’ opened its first Australian pop-up at the 2026 Australian Open in Melbourne. This format of short-term retail space reduces exposure while delivering meaningful data on consumer demand. Leveraging its strong reception at the Australian Open, Shake Shack is rumoured to be planning to open a flagship store in Australia.

International luxury retail

In Melbourne’s ‘Paris end’ of the CBD, Rodd & Gunn’s flagship store opened its first fine-dining restaurant. The brand specialises in premium menswear apparel, originating in New Zealand before expanding to Australia in 1995. The in-store restaurant has now branched into fine dining, offering diners a menu crafted by a Michelin-star chef and paired with a curated wine list.

The Australian luxury retailing industry has thrived over the past few years, which has encouraged international fashion houses like Louis Vuitton to expand their physical footprints, especially in Sydney and Melbourne.

Australian retailers took note when Louis Vuitton launched its Seoul restaurant – a format reminiscent of Rodd & Gunn’s approach. Helmed by a two-Michelin-star chef, the restaurant crowns the brand’s six-storey flagship, spanning its top two floors. Photos show the sophisticated interior with skyline views, Louis Vuitton tableware and carefully curated heritage objects. The restaurant doubles as a showcase for homeware goods, a category luxury brands like Louis Vuitton expanded into during the pandemic as consumers redirected spending toward their living spaces.

Australian shoppers can only watch and wait; however, the success of Rodd & Gunn’s dining venture has proven the appetite exists for this type of luxury experiential retail.

Retail emergence as real estate’s strongest performer

We are witnessing a resurgence of capital appetite for Australian retail property from local and offshore capital sources. Liquidity for larger centres has been supported by several recent transactions; both to existing and new entrant capital sources.

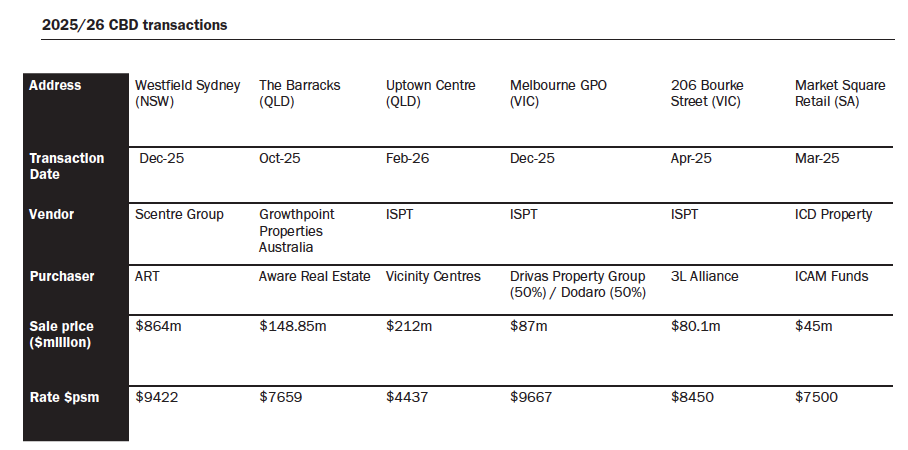

The CBD sub-sector has been no exception, with strong transaction volumes of ~$1.9 billion in the 12 months ending Mar-26, some 90% above the prior 10-year average. Capital is acutely focused on irreplaceable assets offering robust income growth – an example of this is ART’s 19.9%, $864 million acquisition of Westfield Sydney for a 4.69% yield.

The pipeline of retailers wanting a presence in the CBD is supporting the rental growth – bringing increased competition from new entrants and existing retailers expanding CBD store sizes – pushing occupancy to recent highs. This ground-up positivity is driving capital sentiment and supporting pricing.

![]()

What to watch in 2026

Bid activity continues to rebound as capital flocks to retail centres with strong fundamentals in location and tenant composition that underpin rental growth.

In 2026, international brands entering Australia include: Alo Yoga (US) in Chatswood Chase; Auntie Anne’s (US), a soft pretzel retailer that has stores in the QVB and Westfield Parramatta; Loro Piana, the luxury Italian retailer opened in Westfield Sydney in early 2026; and Chinese jeweller Chow Tai Fook opened in late March 2026 in Westfield Sydney.

As geopolitical events create turbulent investing environments and restrict international travel, Australia’s retail market is positioned favourably. Domestic tourism presents a significant opportunity for CBD retail as interstate travellers explore Australia’s unique cities and retail offerings.

- This article by Holly Irvine, Research Analyst at JLL was first published in SCN magazine – CBD Guns edition.

Add comment